The Salkku Markets Outlook for Q2 2026 adopts a cautious and neutral stance for global stock markets over the next 12 months, with noticeable deterioration in both the Salkku Coincident Indicator and Salkku Leading Indicator over Q1 after strong 2025Q4.

Executive Summary

Salkku Markets adopts a cautious neutral stance on global equities over the next 12 months. Both the Salkku Coincident and Leading Indicators have deteriorated from strong 2025Q4 levels, reflecting softening current conditions and subdued forward-looking signals amid persistent inflation pressures and shifting monetary policy expectations.

While a robust technology-driven capital expenditure (capex) cycle—particularly in AI infrastructure—provides a significant tailwind, rising inflation expectations and the prospect of central banks holding or even raising rates (rather than cutting) are dampening economic momentum and corporate outlooks. Our machine learning model still projects modestly positive equity returns with only a slim 50.2% probability, underscoring a fragile environment.

Risk assets remain in an expansionary phase of the multi-year cycle, supportive for high-beta sectors such as technology and cryptocurrencies, with the shorter-term cycle also turning speculative. Investors should maintain balanced positioning, monitor inflation and policy developments closely, and consider selective exposure to AI beneficiaries while preparing for elevated volatility.

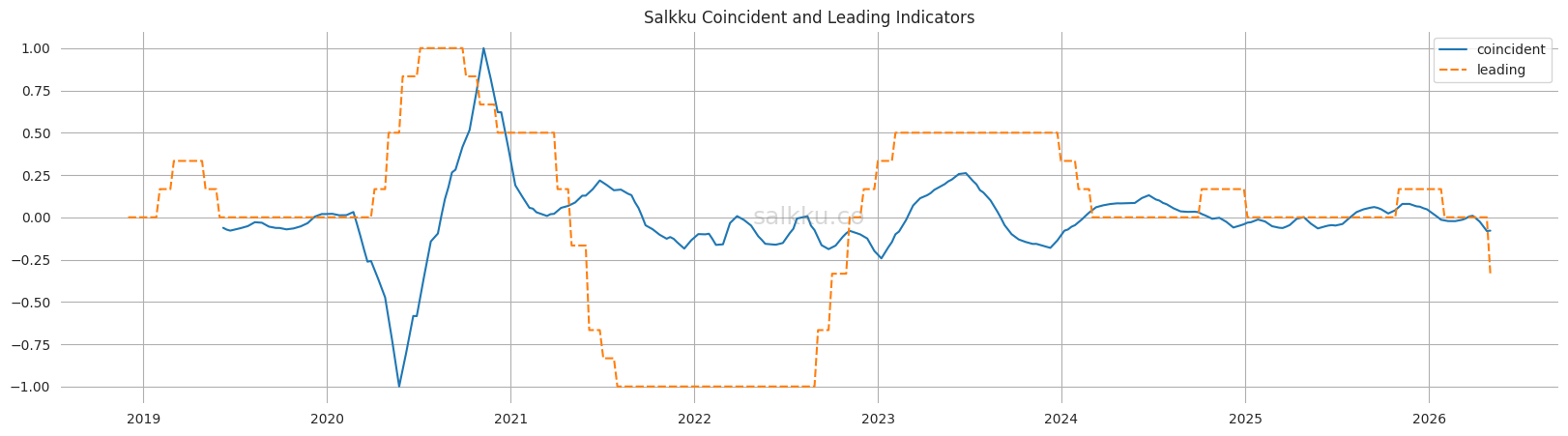

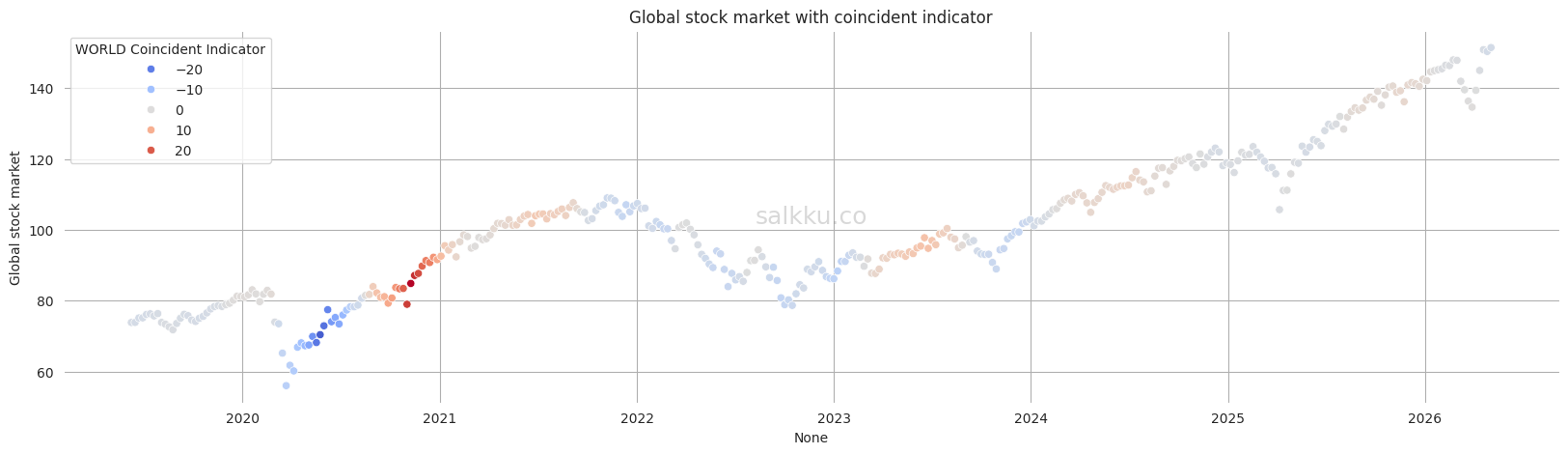

Salkku Coincident Indicator for Global Markets

The Salkku Coincident Indicator tracks the current state of the global economy, primarily through the Composite Global Purchasing Managers’ Index (PMI), which measures business activity in manufacturing and services sectors.

As of early May 2026, the indicator stands at -1.9, marking a notable deterioration from the strong readings in 2025Q4. Recent PMI data shows a mixed picture: the U.S. composite remains in expansion territory (around 51.7–52 in April), while the Eurozone has weakened significantly. Global activity continues to expand modestly overall but at a slower pace than late last year, consistent with broader forecasts of global GDP growth around 3.1–3.3% for 2026.

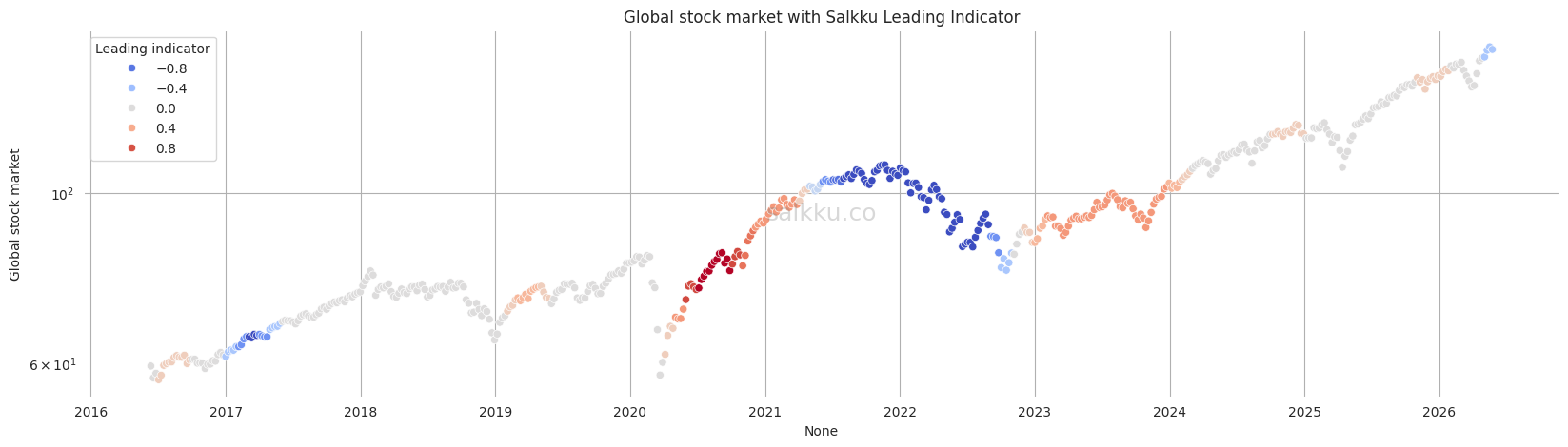

Salkku Leading Indicator for Global Markets

The Salkku Leading Indicator aggregates forward-looking metrics, including economic sentiment, manufacturing orders, and financial market signals, to predict global stock market performance over a 12-month horizon.

In May 2026, the Salkku Leading Indicator registered a negative reading of -0.33, indicating that global stock market returns are expected to be lower than long-term averages over the next 12 months.

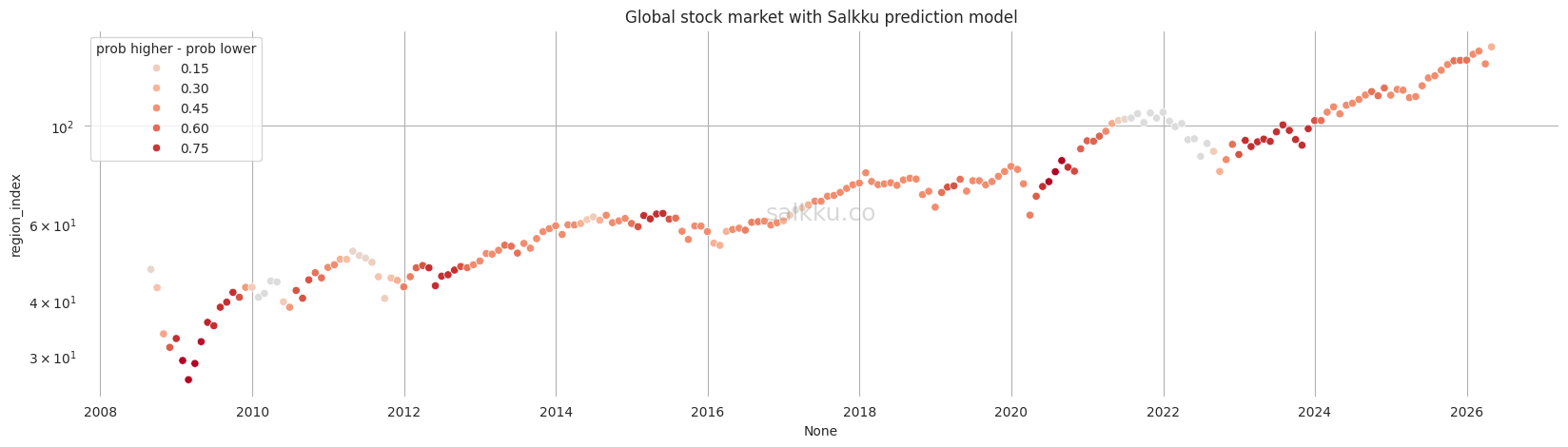

Model Prediction

The global market outlook weakened during 2026Q1. Strong global technology and AI-driven capex investment is being partially offset by a less favorable inflation outlook. Hyperscalers and major tech firms are projected to ramp up capital spending dramatically in 2026 (potentially $500–700 billion collectively), fueling productivity gains and sector leadership. However, higher inflation expectations could prompt central banks to pause rate cuts or even tighten policy, exerting a dampening effect on broader economic activity and prompting companies to temper their 12-month forecasts.

Salkku’s machine learning model nonetheless forecasts positive stock market returns over the next 12 months, albeit with a narrow 50.2% probability. This indicates a fragile baseline vulnerable to adverse shifts in inflation, geopolitics, or capex monetization timelines.

Risk asset cycles

We have identified certain cyclicality in risk assets, which have played out fairly reliably over the past decades. Markets seem to follow a longer term multi-year cycle and shorter multi-month (<1 year) cycle. Risk assets with most beta to this cyclicality are especially tech stocks, and cryptocurrencies, with commodities having a smaller, but non-zero, beta.

Figure 4. is showing a continuation of the most expansionary/speculative phase of the multi-year cycle (in yellow), historically favorable for tech and crypto. The shorter-term cycle has also entered a speculative stage, reinforced by the recent tech rally following April’s dip. When both cycles align in expansion, conditions have typically been especially supportive for high-beta risk assets. Continued monitoring of cycle turning points remains essential.

Overall Recommendation: Maintain a disciplined, diversified approach with emphasis on quality and AI-exposed themes, while hedging against policy and inflation surprises in this balanced but vulnerable environment.